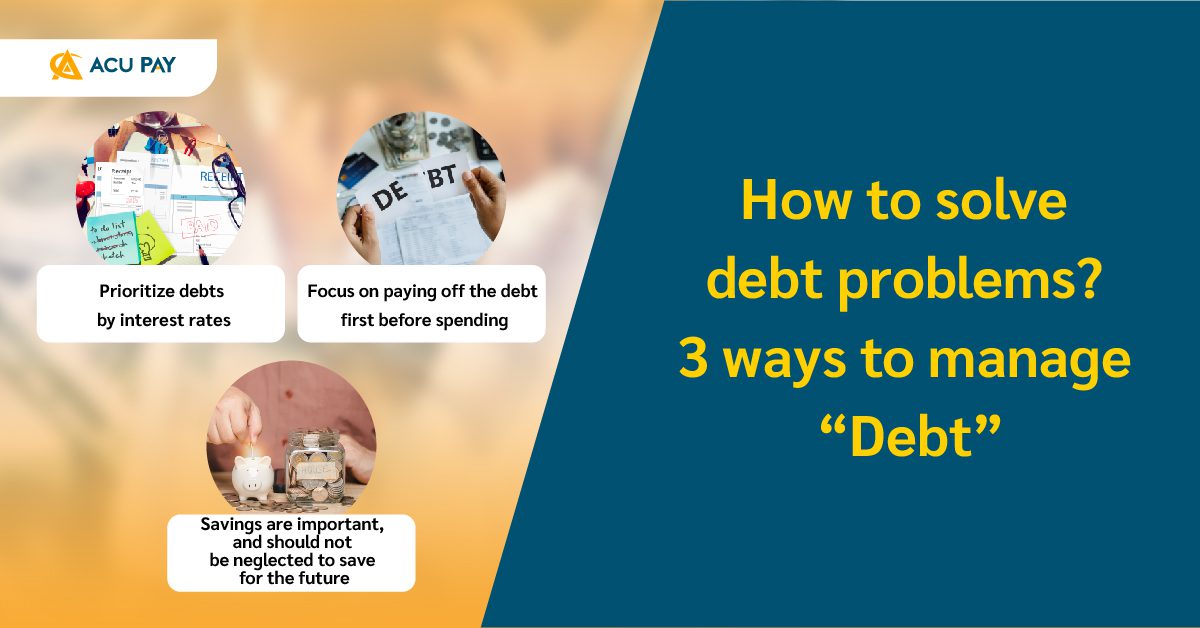

After checking the debt list, the next step to pay off debt is to prioritize the debt and repay the debt with the highest interest or the lowest amount of debt first, including the debt at high risk of property confiscation so that it does not affect your financial status. Certain debt types may have a greater impact than others, such as those at risk of asset confiscation. You may consider the interest rates of each type of debt, such as closing informal debts first because interest rates are higher than those in the system, and then finding a way to repay debts in system with the high interest rates such as cash card or credit card.

If there are multiple debts to be paid, the top priority debt should be closed as soon as possible. You may focus on paying the principal first so that you can repay them faster because the faster and more the principal amount decreases, the lower the interest rate. Once the first debt is closed, then you move to close the next debt and keep doing this until all debts are gone. Many people may want to spend money to reward themselves whether for watching a new movie or celebrating with friends at a restaurant. It will give them the chance to spend all the money until they can’t find a way to repay their debts.

You all know that the key benefit of saving is long-term security and wealth. It’s a way to get you out of life uncertainty and increase the opportunity to improve your quality of life as you want. However, the first thing you should focus on is paying off all your debt, and don’t forget to save up for emergencies because there may be unexpected events that can occur anytime such as sudden unemployment or when family members are sick. If you don’t have any savings, you will have to get a new loan inevitably. It’s even more complicated to pay off your debt. The way to save money for people who have debts is simple, just save at least 3% of their income regularly and deposit it in a high-yield savings account or deposit it in a fixed deposit account. It’s not recommended to invest in stocks or mutual funds because there is a risk of losing the principal.

There are many ways to manage debt depending on individual proficiency. A default also has an impact on financial credit and increases the interest we have to pay in the future. Taking out a loan in the future may be more difficult. For example, if you plan to save money for a house or buy a car, you may want to get a loan. However, when financial institutions check your financial credit and find that they have previously had a history of defaulting, they are unlikely to be able to apply for loans.

References from

makebykbank

MAKE A GREAT DAY WITH ACU PAY.