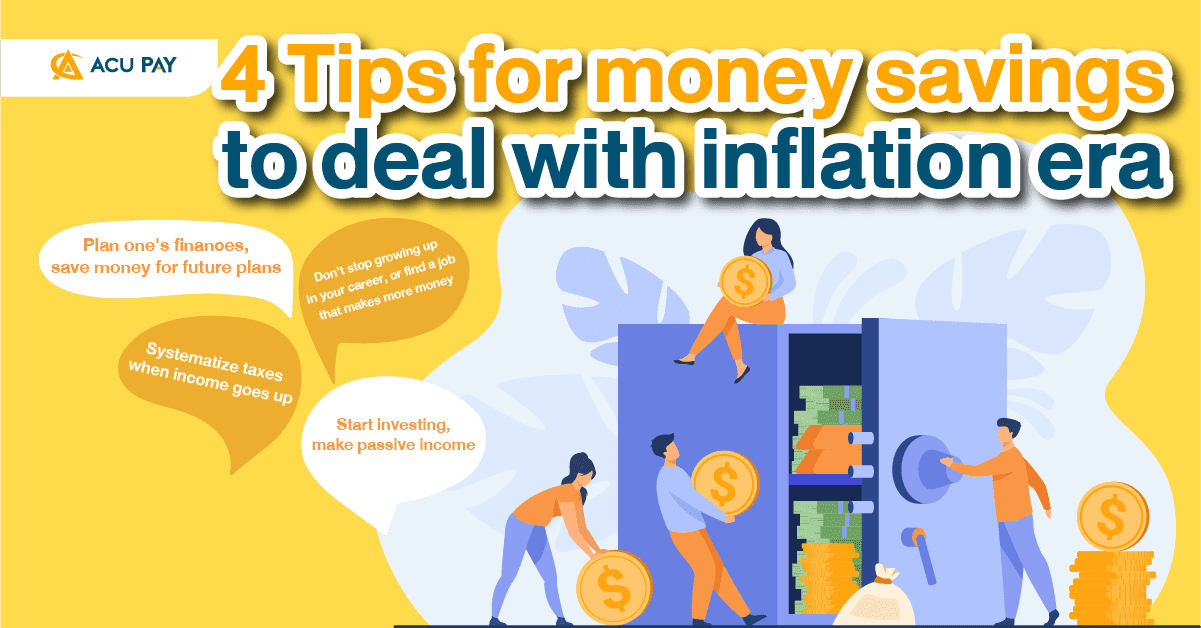

Have you ever planned for money saving, however, your money is still insufficient for you to use? Inflation makes everything more expensive, but our income is still the same which results in our income not being compatible with our expenses. What savings plan is good for us in the inflation era like this? Today, ACU PAYwill share 4 good savings tips with you.

Inflation is an economic situation in which goods and services are priced higher. This means that we buy less but have to pay more expensive, while salaries are not adjusted according to inflation rates. From having a meal that cost 30 baht in the past, we have to pay for our meal at a more expensive price which is 50 baht, resulting in a lower quality of life. Some people may have to borrow money to cover their daily expenses.

Savings tricks to deal with inflation can be applied appropriately as follows:

The first major financial planning step is “saving money,” which requires an effort to cut unnecessary expenses and have consistent savings. For beginners who are just starting to work, don’t be discouraged that you don’t have much money. Gradually saving will help build savings discipline. As you become more stable in your career, your income will increase. Creating savings habits from the start will help you to plan and cope with unexpected events.

The recommended savings plan is to save at least 10% of monthly income and then deposit some money to banks that offer interest rates close to inflation rate. In most cases, the higher inflationary pressure, spending, or investment will be more risky than in normal economic times. Therefore, saving money is an alternative to keeping money. It is recommended to deposit in fixed deposit accounts which will receive relatively high interest rates, including lump sum deposits and the same amount of deposits every month.

The more we try to increase our skills, the more we earn. The more we have outstanding performance, the more chances we have to raise income within a few years. Therefore, not continuing to develop oneself will open up new opportunities. We may choose further study, reading, or learning online courses to enhance our skills. Those skills may also help transform into our supplementary careers to generate more income, as well as being a good alternative to investing in ourselves.

Taxes are often the closest thing that causes a headache to many people and we tend to overlook them. Tax planning is something that we need not worry about at the beginning of the work, but with higher income, the tax ceiling may rise as well. Tax planning can help us reduce our annual expenditures and can reduce taxes as well such as buying a provident fund.

Making additional income in addition to our fixed salary or active income will help us to get closer to financial independence. Investment is an alternative to creating a passive income.

Many people think it’s enough to just deposit money in a bank, but the fact is that depositing money in a bank during high inflation will bring down interest rates or real yields.

For example, 1.25% interest on bank deposits. If inflation is 1%, the real interest rate will be 0.25%.

If interest rates are the same at 1.25%, but inflation increases at 2%, then the real interest rate from bank deposits will be negative (-0.75 %).

This is why it is important to study investments that yield returns, from debentures, debt instruments, funds, and stocks, each of which yields different returns. Particularly during inflation, it is recommended that if investors choose to invest in long-term debt instruments, they should not hold too long of long-term debt instruments because they may lose value from their holdings that have been adjusted according to the policy rate. For stocks, you may choose stocks that do not move much in line with the economic situation and stocks that are essential to daily life.